LendingTree Personal Loan Offers Report

Rate and loan-amount offers varied widely among consumers, depending on factors including (but not limited to) credit score, income and current debt obligations.

-

Spreads between the highest and lowest offered APRs ranged from 1,064 basis points for the highest-score borrowers, and 1,367 basis points for the bottom end of the prime scores.

- The average spread for those with scores of 760 or higher was 1,064 basis points, amounting to a difference of 57%, or $3,641, on the average loan amount offered to this credit band for a three-year personal loan.

- Consumers with scores between 720 and 759 saw an average offer spread of 1,119 basis points, representing a 49%, or $3,101, average difference in interest paid.

- For those with scores between 680 and 719, the average spread was 1,143 basis points, representing a 42%, or $2,613, difference in interest paid.

- Borrowers with scores between 640 and 679 had an average spread of 1,367 basis points, representing a 41%, or $2,435, difference in interest paid over the three years of a typical

-

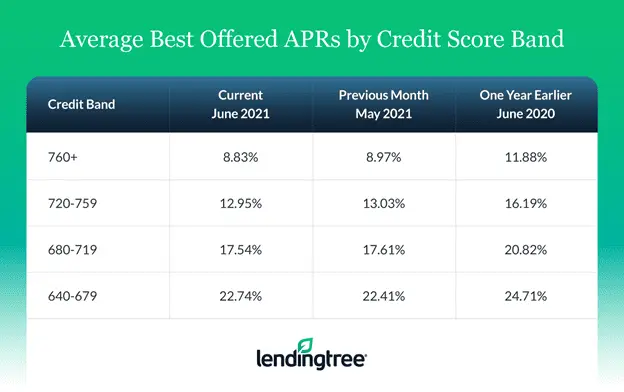

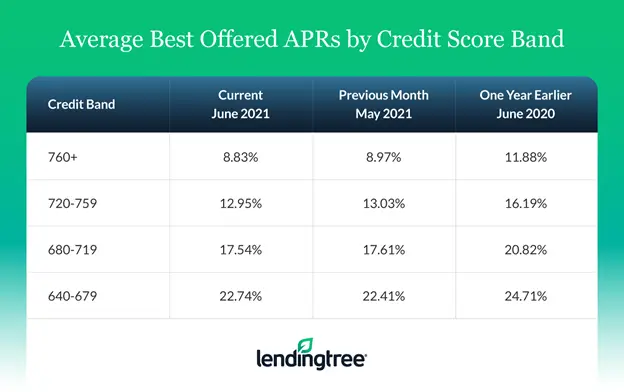

Excellent credit (760+ score): Best offered APRs to consumers averaged 8.83% in June.

- The average best APR offered to all borrowers with credit scores of 760 or above was 8.83%, a decrease of 14 basis points from the prior month, and a decrease of 305 basis points from the same period one year ago.

- At $20,128, the average loan amounts offered with the best APRs to all borrowers with a score of 760 was down 6% ($1,246) from last month, and also down 7% ($1,389) from the same period one year ago.

- The top 10% of offers, presented to borrowers with the best profiles within this group, had offered APRs of 4.16% on average, and an average loan amount of $24,963. A borrower with this APR and loan amount would save $4,018 by consolidating debt with a 10% APR over a three-year term.

-

Good credit (680- 719 score): Best offered APRs averaged 17.54% in June.

- The average best APR for all borrowers with credit scores of 680– 719 was 17.54%, a decrease of 7 basis points from last month, and down 328 basis points from a year earlier.

- At $9,818, borrowers with scores of 680- 719 saw the amounts offered with the best APRs decrease by 2% ($166) in the last month, and decrease by 52% ($5,067) from the same period last year.

- The top 10% of offers, presented to borrowers with the best profiles within the 680– 719 credit score range, had an average best APR of 7.86%, offered with an average loan amount of $14,736. A borrower with this APR and loan amount would save $3,636 by consolidating debt from a 15% APR over a three-year term.

- The most common reasons for seeking a personal loan are credit card refinancing and debt consolidation. These two categories comprised 47% of sampled loan inquiries in June.

About the Report

The LendingTree Personal Loan Offers Report contains data from actual 36-month loan terms offered to borrowers with credit scores of at least 640 on LendingTree.com by third-party lenders. Our report averages the best offered APRs by credit score band and the best 10% of offered APRs within each credit score band, as well as the average loan amounts that accompanied those offers. Separately, we average the differences between the highest and lowest APRs offered to each consumer within each credit band and calculate the difference in interest paid that would represent the average loan amount offered within that credit band on a three-year term.

We organize results by credit score so that borrowers have added information about how their credit profiles can affect their loan prospects. We present the offers spread to demonstrate the variety in terms offered to the same consumers.

The personal loan market is a fundamental component of personal finance products available to consumers, and personal loans are often used to refinance existing debt. Knowledge about the terms available to similar borrowers can be a key to making decisions about managing personal finances. We believe this report is an important addition to standard industry surveys and reports on personal loan rates, as most quoted industry rates are either the minimum possible rate or the average rate, and few borrowers will experience either.

Get personal loan offers from up to 5 lenders in minutes