Homeownership in the Nation’s Largest Metros Is an Achievable Goal for the Majority of the Middle Class

Americans frequently hear about issues that impact the “middle class.” Unfortunately, while the term might be an easy buzzword for politicians and their campaigns to use, it isn’t very specific. As a result, discussions on the middle class often ignore all the variety that exists within the group.

A family can be considered part of the of the middle class if their household earns between two-thirds to double the national median income, after incomes have been adjusted for household size, according to the Pew Research Center. Obviously, people on the ends of this spectrum can experience significantly different challenges in their day-to-day lives, so it doesn’t necessarily make sense to always lump them into the same category.

With that in mind, LendingTree decided to examine the issue of housing affordability for different ends of the middle-class spectrum. Economists continue to be concerned with rising homeownership costs and whether they are unaffordable to many middle-class Americans. But this is difficult to determine because of how the middle class is defined.

To better understand the true picture, LendingTree, one of the nation’s largest online loan marketplace, has taken a more nuanced look into whether or not middle class families struggle to afford homes. We did this by breaking up members of the middle class into three subgroups: Lower-Middle Class (those who make two-thirds of the median income), Middle-Middle Class (those who make exactly the median income) and Upper-Middle Class (those who make double the median income).

By looking at the middle class in this way, we were able to better understand home affordability in the nation’s largest metros.

Key findings

- In most metros, buyers who make the median income can afford a median-priced home in their area. This is good news, as it means that most metros aren’t prohibitively expensive for the majority of the middle class. In fact, we found that, on average, a middle-middle class family makes about $450 dollars more a month than what would be necessary to pay for a home priced at the median home value in their area. An upper-middle class family makes more than $1,900 above what would be necessary to pay for a median-value home.

- Lower-middle class families can still afford a median-priced home in 34 of the nation’s largest metros. Furthermore, even if they can’t afford a median priced home, there are still many housing options available for lower-middle class families in most of the nation’s largest metros.

- Houston, Dallas and Minneapolis are the metros where members of the middle-middle class have the easiest time paying for a median priced home. In these metros, middle-middle class families could afford to pay almost $800 more than what they need to pay in order to purchase a median priced home.

- Upper-middle class families have the easiest time affording a median priced home in Washington, D.C., Minneapolis and Hartford, Conn. While there is no metro in our study where upper-middle class families cannot afford a median priced home, in these three metros, they can afford to spend about $2,600 more than what they would need to pay for a median priced home.

- Houston, Pittsburgh and Buffalo, N.Y. are the metros where lower-middle class families have the easiest time purchasing a home. In these metros, lower-middle class families can afford to pay nearly $300 more than what they would need to pay in order to be able to afford a median-priced home.

- The metros that are least affordable for the entire middle class are all in California. The lower- and middle-middle classes face the most difficulty affording a home in Los Angeles, San Francisco, and San Jose, Calif. For the upper-middle class, the least affordable metros are Los Angeles, San Diego and San Jose, Calif. However, families in the upper-middle class still make more than enough money to comfortably pay for a home in any of the nation’s 50 largest metros.

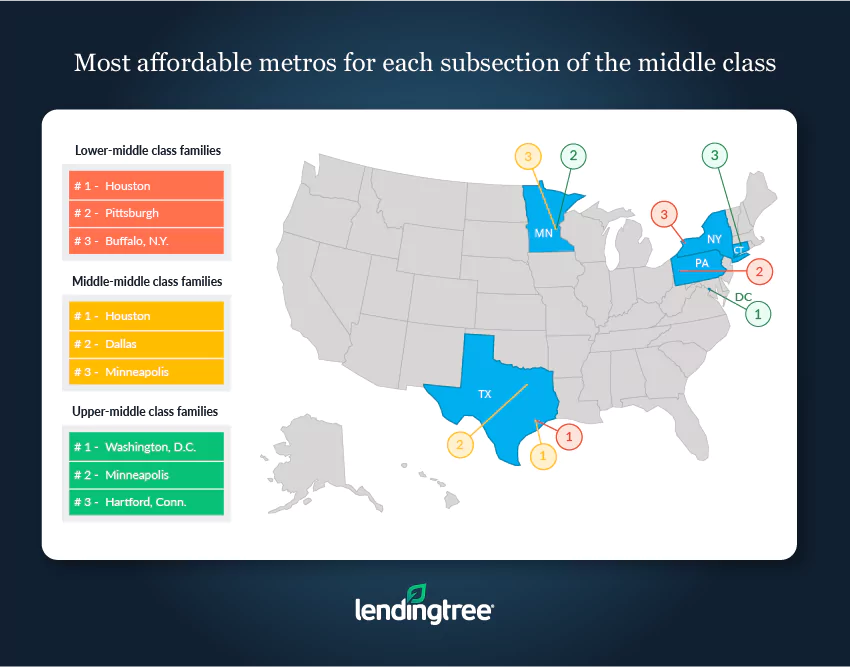

Most affordable metros for lower-middle class families

No. 1: Houston

- Median home price: $166,500

- Lower-middle class income: $41,948

- Likely monthly payment for a median priced home: $683

- Affordable monthly payment for a lower-middle class family: $979

- Monthly payment surplus: $296

No. 2: Pittsburgh

- Median home price: $142,100

- Lower-middle class income: $37,382

- Likely monthly payment for a median priced home: $583

- Affordable monthly payment for a lower-middle class family: $872

- Monthly payment surplus: $289

No. 3: Buffalo, N.Y.

- Median home price: $135,000

- Lower-middle class income: $35,689

- Likely monthly payment for a median priced home: $554

- Affordable monthly payment for a lower-middle class family: $833

- Monthly payment surplus: $279

Most affordable metros for middle-middle class families

No. 1: Houston

- Median home price: $166,500

- Middle-middle class income: $62,922

- Likely monthly payment for a median priced home: $683

- Affordable monthly payment for a middle-middle class family: $1,468

- Monthly payment surplus: $785

No. 2: Dallas

- Median home price: $174,500

- Middle-middle class income: $63,870

- Likely monthly payment for a median priced home: $716

- Affordable monthly payment for a middle-middle class family: $1,490

- Monthly payment surplus: $775

No. 3: Minneapolis

- Median home price: $230,700

- Middle-middle class income: $73,735

- Likely monthly payment for a median priced home: $946

- Affordable monthly payment for a middle-middle class family: $1,720

- Monthly payment surplus: $774

Most affordable metros for upper-middle class families

No. 1: Washington, D.C.

- Median home price: $397,900

- Middle-middle class income: $194,296

- Likely monthly payment for a median priced home: $1,632

- Affordable monthly payment for a middle-middle class family: $4,534

- Monthly payment surplus: $2,902

No. 2: Minneapolis

- Median home price: $230,700

- Middle-middle class income: $147,470

- Likely monthly payment for a median priced home: $946

- Affordable monthly payment for a middle-middle class family: $3,441

- Monthly payment surplus: $2,495

No. 3: Hartford, Conn.

- Median home price: $244,300

- Middle-middle class income: $146,418

- Likely monthly payment for a median priced home: $1,002

- Affordable monthly payment for a middle-middle class family: $3,416

- Monthly payment surplus: $2,415

What this means

As our study shows, median-priced homes are affordable to the majority of middle-class families. Of course, this does not necessarily mean that everyone in the middle class can afford a median-priced home in the area that they live in.

Just as middle-class families may have different incomes, they may also have other expenses that can take away from the money necessary to purchase a home, like student loan debt and child care costs. Furthermore, while 20% is a standard down payment, it isn’t necessarily feasible for everyone.

As a result, some families may need to spend more time than others in saving up for a down payment, or strengthening their credit score in order to get a more favorable interest rate. Beyond that, some families may want to consider alternative options to help them pay for a home, from budgeting to spend more than 28% of their income on housing costs, or considering applying for special government programs like FHA loans that can help lower housing cost burdens.

Methodology

When determining whether or not a home is affordable, we assume that the a middle class buyer will be able to afford a 20% down payment on the medium home value in their area, and that they will receive a mortgage loan with a rate of 4.6% (the average rate offered to Americans). By using that data, we calculated the likely monthly down payment for a median priced home in a given metro.

We calculate an “affordable” monthly mortgage payment based on the “28% rule,” which says that a person should not spend more than 28% of their yearly gross income on yearly costs related to housing. This rule, while not necessarily applicable to everyone, is useful for homebuyers to keep in mind, as it helps to ensure that they are not overspending on their home and leaving too little money for other expenses.

By subtracting the monthly housing payment that is affordable to a person making a median income from the calculated housing payment that would be required to purchase a home valued at the median level, we are able to determine whether or not the average person can afford to purchase a home in the metro that they live in.

View mortgage loan offers from up to 5 lenders in minutes