Snapshots of Black and White Disparities in Income, Wealth, Savings and More

Racial disparities have always existed with finances. With February being Black History Month, LendingTree researchers updated this compilation of data on income, wealth, savings, employment and credit to provide snapshots of Black and white economic inequality.

Here’s what we found.

Key findings

- The median income for Black households in the U.S. is 33.3% lower than that of white households. Black households earned a median of $56,490 in 2023, compared with $84,630 among white households. This is a slight increase from the 31.6% gap in 2022 — $52,860 versus $77,250.

- Full-time Black workers’ median weekly wages are 18.8% lower than those of full-time white workers. Black workers earned a median of $962 weekly in the third quarter of 2024, versus $1,184 among white workers. As of March 2024, full-time Black workers in the agricultural industry made an average of 40 cents for every dollar their full-time white colleagues earned — the lowest among the sectors tracked.

- Black Americans have $5.39 trillion in wealth, compared with the $134.58 trillion held by white Americans. As of the third quarter of 2024, white Americans hold 84.2% of the country’s wealth, while Black Americans hold 3.4%, despite representing 58.4% and 13.7% of the population, respectively.

- About 2 in 3 Black adults say they’re doing OK financially. 68% of Black adults said this about their finances in 2023, up from 64% in 2022. That compares with 76% of white adults in 2023, down from 77% the year before.

- A higher rate of Black adults say they or another household member suffered a recent loss of employment income. 16.0% of Black adults said this from Aug. 20 to Sept. 16, 2024, about the prior four weeks, versus 10.3% of white adults.

- Black adults with lower incomes are far more likely to be denied credit or approved for less than requested than their white counterparts. As of 2023, 65% of Black adults with a family income of less than $50,000 who applied for credit in the prior 12 months were denied or approved for less than requested, compared with 47% of white adults in the same income group.

Income

The Black and white income gap across the U.S. has remained substantial since 1970:

- 1970: The median income for Black households (in 2018 dollars) was $30,400, according to the Pew Research Center. That’s compared with $54,100 for white households — a difference of $23,700, or 43.8% less.

- 2023: The median income for Black households was $56,490, according to the U.S. Census Bureau Current Population Survey (CPS) 2024 Annual Social and Economic (ASEC) Supplement. That’s compared with $84,630 among white households — a difference of $28,140, or 33.3% less.

Household income nationally (2022)

| Median | Avg. | |

|---|---|---|

| White | $84,630 | $118,000 |

| Black | $56,490 | $80,710 |

| Difference ($) | -$28,140 | -$37,290 |

| Difference (%) | -33.3% | -31.6% |

This compares to a 35% gap in median household incomes in 2021. The median income for Black households was $48,297 that year, compared with $74,262 for white households.

In the third quarter of 2024, median weekly wages for full-time Black workers equaled 81.3% of the wages earned by full-time white workers, according to an analysis of U.S. Bureau of Labor Statistics (BLS) data. That breaks down to $962 versus $1,184 — a difference of $222 a week, or $11,544 a year.

Average earnings vary widely by industry and race. For example, Census Bureau data shows that full-time Black workers in the agriculture industry earned $400 a week as of March 2024, while full-time white workers in that same industry earned $991 a week. That means Black agriculture workers made 40 cents for every dollar earned by their white colleagues.

In just two sectors — leisure and hospitality, and information — the weekly wages for Black workers are higher than those for white workers: $986 versus $961, and $1,763 versus $1,743.

How weekly wages vary by industry and race

| Industry | Wages, white workers | Wages, Black workers | Difference ($) | Difference (%) | Cents on dollar |

|---|---|---|---|---|---|

| Information | $1,743 | $1,763 | $20 | 1.1% | $1.01 |

| Financial activities | $1,558 | $1,428 | -$130 | -8.3% | $0.92 |

| Public administration | $1,502 | $1,228 | -$274 | -18.2% | $0.82 |

| Professional and business services | $1,615 | $1,202 | -$413 | -25.6% | $0.74 |

| Manufacturing | $1,378 | $1,194 | -$184 | -13.4% | $0.87 |

| Transportation and utilities | $1,436 | $1,152 | -$284 | -19.8% | $0.80 |

| Construction | $1,244 | $1,123 | -$121 | -9.7% | $0.90 |

| Educational and health services | $1,366 | $1,009 | -$357 | -26.1% | $0.74 |

| Leisure and hospitality | $961 | $986 | $25 | 2.6% | $1.03 |

| Other services | $1,138 | $977 | -$161 | -14.1% | $0.86 |

| Wholesale and retail trade | $1,118 | $890 | -$228 | -20.4% | $0.80 |

| Agriculture, forestry, fishing and hunting | $991 | $400 | -$591 | -59.6% | $0.40 |

Wealth

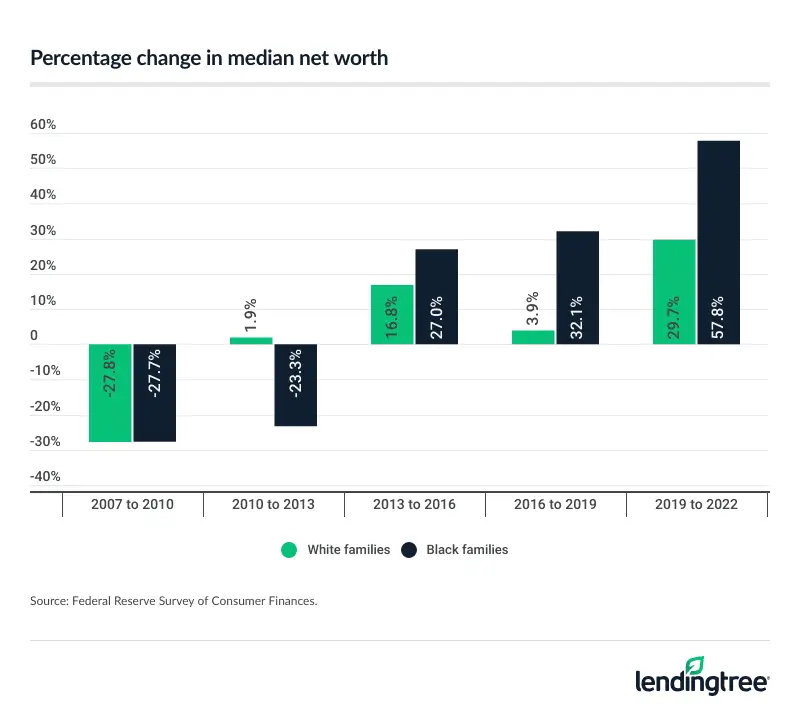

Median net worth for Black and white families continues to fluctuate, according to Federal Reserve Survey of Consumer Finances data, though the gap remains massive:

- Black and white families saw similar 27.7% and 27.8% drops in median net worth from 2007 to 2010 amid the Great Recession of 2007 to 2009. The median net worth for Black families went from $30,050 to $21,720, while the median net worth for white families went from $245,450 to $177,210.

- Between 2010 and 2013, the median net worth for Black families saw another significant decrease (23.3%) to $16,650, while white families’ net worth rebounded 1.9% to $180,620.

- Between 2013 and 2016, though, the median net worth for Black families dramatically increased by 27.0% to $21,150. It jumped 16.8% (to $210,910) for white families.

- That growth continued between 2016 and 2019, with median net worth rising 32.1% (to $27,940) for Black families and 3.9% (to $219,210) for white families.

- Between 2019 and 2022, the median net worth for Black families skyrocketed by 57.8% to $44,100, while the median net worth for white families spiked by 29.7% to $284,310.

That said, the difference in median net worth among Black and white families increased from $155,490 in 2010 after peaking in the lead-up to the Great Recession to $240,210 in 2022.

It’s good there’s been some median wealth growth among Black families, says LendingTree chief consumer finance analyst Matt Schulz, but he notes that data may not paint the whole picture.

“It may tell you more about where these two groups were starting from than anything else,” he says. “That’s because it’s a lot easier to have high-percentage growth when starting with a low income number than when starting with a big income number.”

In other words, if you used to make $20,000 and get a $5,000 raise, it marks a far bigger percentage increase than if you make $100,000 and get a $5,000 raise. Either way, Schulz says, a $5,000 raise is great, but it’s likely much more significant to the person who started with the smaller income.

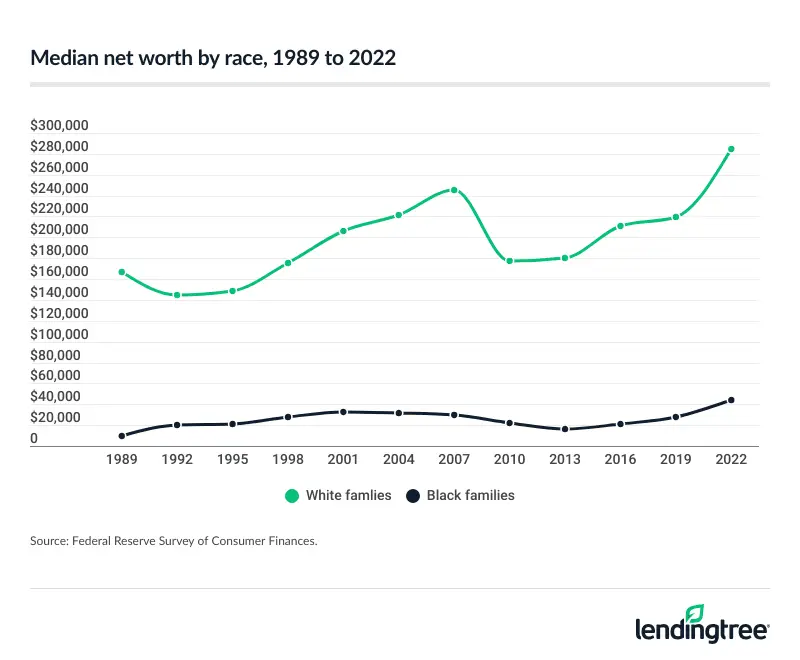

The data suggests similarly. In fact, Black families’ median and average net worth in 2022 was considerably lower than that of white families.

Net worth among families

| Median net worth | Average net worth | |||

|---|---|---|---|---|

| Black families | White families | Black families | White families | |

| 1989 | $9,910 | $166,420 | $95,670 | $533,320 |

| 1992 | $20,510 | $144,420 | $99,800 | $462,080 |

| 1995 | $21,130 | $148,640 | $85,160 | $488,520 |

| 1998 | $28,260 | $175,000 | $116,840 | $617,770 |

| 2001 | $32,310 | $205,740 | $119,960 | $818,570 |

| 2004 | $32,050 | $221,500 | $176,500 | $884,570 |

| 2007 | $30,050 | $245,450 | $192,400 | $991,120 |

| 2010 | $21,720 | $177,210 | $135,590 | $886,600 |

| 2013 | $16,650 | $180,620 | $126,040 | $886,540 |

| 2016 | $21,150 | $210,910 | $170,270 | $1,146,830 |

| 2019 | $27,940 | $219,210 | $164,990 | $1,136,660 |

| 2022 | $44,100 | $284,310 | $211,600 | $1,361,810 |

Black Americans had far less wealth as of the third quarter of 2024, according to the Federal Reserve. Black Americans held 3.4% — or $5.39 trillion — of the country’s wealth, versus 84.2% — or $134.58 trillion — among white Americans. This doesn’t align with the population, according to the Census Bureau. Black and white Americans represent 13.7% and 58.4% of the population, respectively.

Savings

In 2023, 14% of Black adults were unbanked, according to the Federal Reserve, while just 4% of white adults said the same. (Unbanked refers to respondents or their spouses without a checking, savings or money market account.)

Black Americans with bank accounts are more than twice as likely to incur an overdraft fee as white Americans — 19% versus 9%.

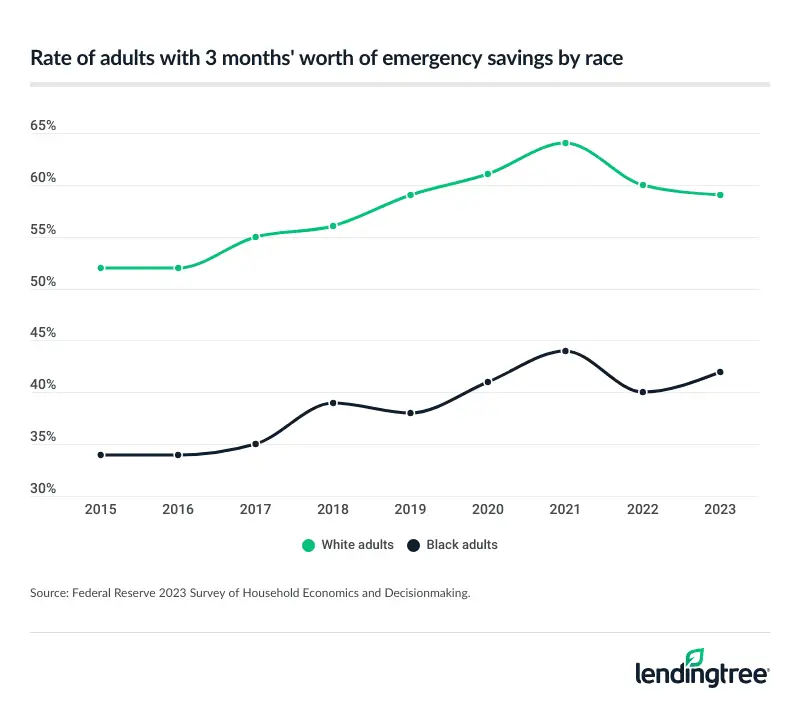

According to the Federal Reserve, 59% of white adults had three months of emergency savings in 2023, compared with 42% of Black adults.

“Black households have less financial margin for error than white households in many cases because of income disparities,” Schulz says. “This is a big problem anytime, but it’s particularly troubling in times of inflation. Higher prices mean that people have even less wiggle room financially. That means less money to put toward paying down credit card debt, growing their emergency fund or contributing to savings for college, a mortgage or other big goals.”

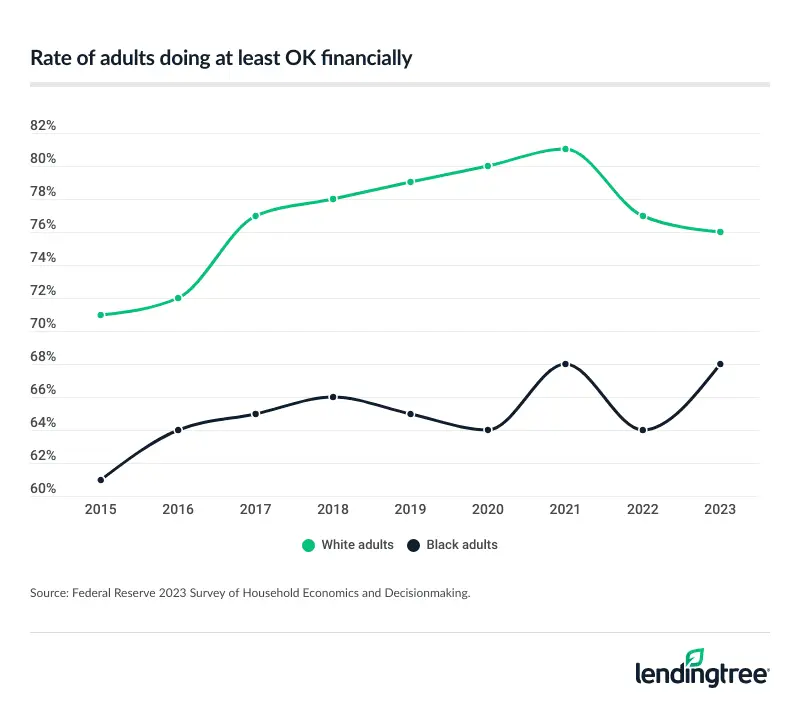

Overall, 68% of Black adults said they were doing OK financially in 2023, according to the Federal Reserve, up from 64% the previous year and 53% in 2013. Meanwhile, 76% of white adults said they were OK financially, down from 77% in 2022 and up from 65% in 2013.

For those looking for a boost despite the tumultuous market, Schulz recommends looking for a high-yield savings account.

“For many years, savings accounts gave savers minuscule returns,” he says. “That’s not the case anymore. You can find savings accounts with APYs of 4% or higher, though you’ll likely have to look beyond the traditional megabanks. Recent Fed rate cuts mean the days of getting 5% or higher returns are probably gone — and further cuts later this year could lower returns further. It’s still worth your time to shop for a high-yield savings account.”

Employment

Black adults report feeling the effects of employment income loss more than white adults. Overall, 16% of Black adults in August and September 2024 said they or another household member suffered a loss of employment income in the past four weeks, according to Census Bureau data, while 10% of white adults said the same.

It’s not the first time something like this has happened, either. In fact, minorities — according to research — have historically been affected by a “last-hired, first-fired” phenomenon. In other words, racial and ethnic minority groups during an economic downturn are typically among the first laid off. During an economic recovery, however, they’re among the last hired.

That’s had an impact on the unemployment disparity, too. As of December 2024, the unemployment rate for white men and women ages 20 and older was 3.3% and 3.4%, respectively, according to the BLS. Meanwhile, it was 5.6.% and 5.4%, respectively, for Black men and women in the same age group.

Credit

In 2023, 65% of Black adults with a family income of less than $50,000 who applied for credit were denied or approved for less than they requested, according to the Federal Reserve, compared with 47% of white adults. Meanwhile, more than 1 in 4 Black applicants (29%) from families making $100,000 or more a year had their credit applications denied or approved for less in 2023, compared with 13% of white adults in the same bracket.

In 2023, 86% of white adults had a credit card, while only 70% of Black adults had one.

According to Schulz, the fact that Black applicants are likely to have lower incomes may hold them back from higher credit limits.

“As for getting approved for less than requested, there’s no question that income levels play a big role,” he says. “While your income level isn’t factored into your credit score, it’s considered when, for example, banks decide how much credit to extend. People with higher incomes may receive higher limits on credit cards than those with lower incomes, all other things being equal.”

If you’re overwhelmed by your debt and unable to make on-time payments, Schulz suggests consolidating debts with a personal loan.

“Low-interest personal loans are amazing,” he says. “They can not only help you save a ton of money in interest payments, but they can help you streamline your to-do list. Use a personal loan to pay off several smaller debts so you’ll only have one debt payment to manage instead of wrestling with several simultaneously.”

Retirement

Just more than 1 in 3 (34.8%) Black families had retirement accounts — including 401(k) and individual retirement accounts — in 2022, while 61.8% of white families had them.

Retirement accounts by race

| Median retirement account value | Avg. retirement account value | |||

|---|---|---|---|---|

| Black families | White families | Black families | White families | |

| 1989 | $13,830 | $27,670 | $42,920 | $92,430 |

| 1992 | $11,400 | $31,080 | $40,660 | $98,970 |

| 1995 | $15,480 | $35,030 | $43,200 | $119,490 |

| 1998 | $20,060 | $47,410 | $58,630 | $147,540 |

| 2001 | $14,230 | $58,930 | $53,980 | $196,220 |

| 2004 | $23,570 | $64,420 | $93,840 | $214,870 |

| 2007 | $37,210 | $75,840 | $97,770 | $240,460 |

| 2010 | $24,580 | $73,750 | $72,150 | $264,390 |

| 2013 | $24,180 | $96,740 | $71,670 | $301,160 |

| 2016 | $30,460 | $94,970 | $92,170 | $321,810 |

| 2019 | $40,570 | $92,740 | $126,510 | $341,030 |

| 2022 | $39,000 | $100,000 | $117,530 | $380,330 |

Meanwhile, 51% of Black nonretired adults have tax-preferred retirement savings accounts as of 2023, compared to 68% of white nonretired adults.

Sources

- U.S. Census Bureau Current Population Survey (CPS) Annual Social and Economic (ASEC) Supplement

- U.S. Bureau of Labor Statistics (BLS)

- Federal Reserve Distributional Financial Accounts

- U.S. Census Bureau QuickFacts

- Federal Reserve Economic Well-Being of U.S. Households survey

- U.S. Census Bureau Household Pulse Survey

- Pew Research Center

- Federal Reserve Survey of Consumer Finances

- Federal Reserve Board Survey of Household Economics and Decisionmaking (SHED)

Get debt consolidation loan offers from up to 5 lenders in minutes