Florida, Tesla Borrowers Take Out the Longest Auto Loans

Even if you haven’t shopped for a car in the past few years, you’ve probably heard that prices have skyrocketed. In fact, Americans are borrowing an average of $40,184 for new vehicles and $27,167 for used vehicles, according to the latest Experian data. That’s no small sum to pay back over a short term, so it makes sense that people have been looking for longer car loans.

The newest LendingTree study found that auto loans closed on the LendingTree platform in the past three years had an average term of 65.4 months — nearly five-and-a-half years. We also analyzed auto loan terms by state, metro and brand.

Key findings

- Auto loans closed on the LendingTree platform in the past three years had an average term of 65.4 months. That’s nearly five-and-a-half years. Over the three years analyzed, the highest average was in September 2023 (70.0 months), while the lowest was in November 2020 (59.9). The most common auto loan term nationally was 72 months (45.1%).

- Florida car buyers took out the longest auto loans, at an average of 67.7 months, followed by Oklahoma (67.5) and Louisiana (67.1). Among the states with available data, New York car buyers took out the shortest auto loans (63.7 months), below Kansas (64.5) and Nebraska and Minnesota (tied at 64.6).

- Among the 25 largest U.S. metros, two Florida locales — Orlando (68.9 months) and Tampa (68.4) — took out the longest auto loans, on average. Riverside, Calif., joined in the top three, at 67.6 months. At the bottom were Boston (64.1 months) and Minneapolis and New York (tied at 64.5).

- Portland, Ore., had the highest rate of borrowers taking on auto loans of more than six years, at 17.7%. The two metros with the longest auto loans had the next highest rates of borrowers with these terms — Tampa (16.7%) and Orlando (16.2%). Boston (8.2%) was the only one of the 25 metros below 10.0%.

- Tesla buyers took out the longest auto loans, at 70.0 months, on average. Kia (68.8 months) and Ram (67.9) borrowers followed. Meanwhile, Lexus, Volvo and Mercedes-Benz buyers had the shortest loans, at 62.5, 64.6 and 64.7 months, respectively.

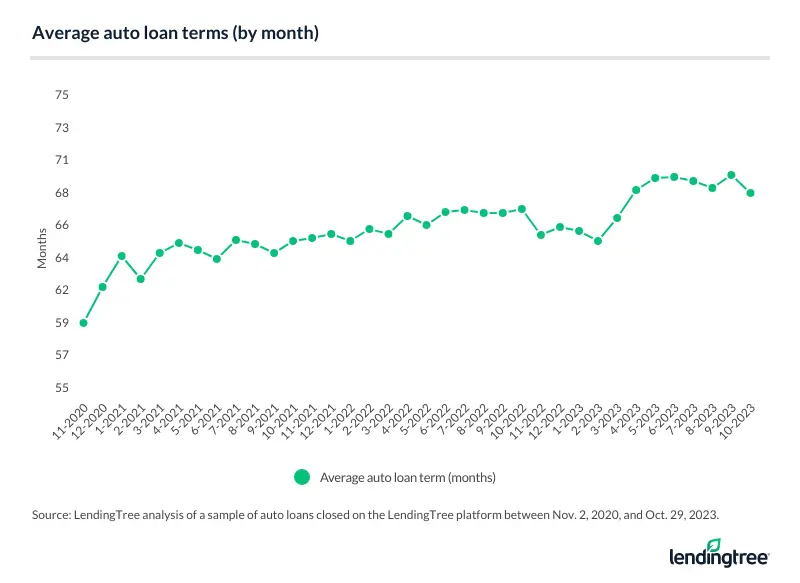

Average auto loan term nationally: 65.4 months

Over the past three years (Nov. 2, 2020, to Oct. 29, 2023), auto loans closed on the LendingTree platform averaged 65.4-month terms.

That’s up from a three-year average of 62.9 months when we last published on this topic in November 2021. (That study covered Oct. 12, 2018, to Oct. 12, 2021.)

Americans’ disposable income has barely budged over the most recent period analyzed. Outside of a few peaks, disposable income levels were generally the same in October 2023 as in November 2020, according to St. Louis Fed data. To combat this and other factors like inflation, Americans are leaning on longer terms. These can come with smaller monthly payments, making vehicles more affordable — though you’ll pay more in the long run.

The time of year and the year itself also impact auto loan terms. For example, the highest average auto loan term in the three years analyzed was in September 2023 (70.0 months), while the lowest was in November 2020 (59.9). Since 2021, average amounts financed and loan rates on new and used vehicles have increased.

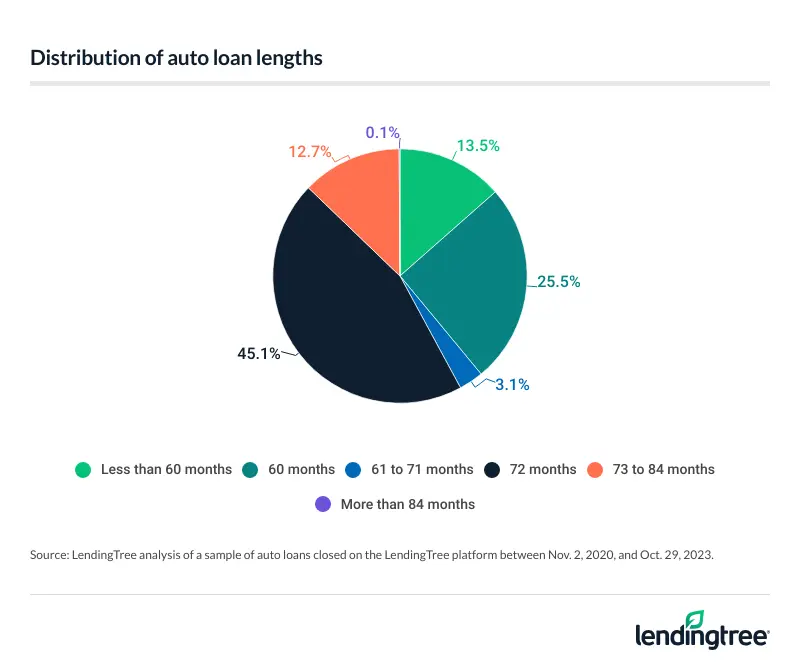

Nationally over the three years analyzed, 45.1% of auto loans were for 72 months (or six years) — by far the highest category. Another 12.8% were for 73 months or longer. That’s significant.

In our last study (which covered mid-October 2018 to mid-October 2021), a smaller percentage of loans were for six years or longer (44.3%) than this year’s percentage for six years alone.

Florida auto borrowers take out the longest loans

Location brings significant differences in auto loan term lengths. For example, Florida car buyers took out the longest auto loans, with an average term of 67.7 months. Next were Oklahoma (67.5) and Louisiana (67.1).

Incomes in these states may not go as far, leaving residents to opt for longer auto loan terms. In fact, each of these states has a below-average median household income compared to the U.S. average:

- Florida: $67,917

- Oklahoma: $61,364

- Louisiana: $57,852

- U.S.: $75,149

And Florida stands out among these states because median gross rent there outpaces the national average — $1,444 versus $1,268.

Researchers excluded states where samples were too low, so only 36 states were considered when compiling our rankings.

Among the states with available data, New York state car buyers took out the shortest auto loans (63.7 months), below Kansas (64.5) and Nebraska and Minnesota (tied at 64.6).

At first glance, New York state’s ranking may seem unusual. The state’s largest city — New York City — is notorious for its high cost of living, after all. But a far lower proportion of people own vehicles in the city compared to the country as a whole. With above-average median household incomes across the state, New Yorkers (in the city or elsewhere) may be better positioned to opt for shorter terms with higher monthly payments.

The other states have multiple factors at play, too. For example, Kansas, Nebraska and Minnesota have lower-than-average median gross rent costs. And Minnesota residents have above-average median household incomes. Residents of these states may be better equipped to save more money than those in higher-ranking states, leading to shorter auto loan terms.

States where consumers take out the longest auto loans

| Rank | State | Avg. auto loan term (months) |

|---|---|---|

| 1 | Florida | 67.7 |

| 2 | Oklahoma | 67.5 |

| 3 | Louisiana | 67.1 |

| 4 | Connecticut | 67.0 |

| 5 | Arizona | 66.7 |

| 5 | Maryland | 66.7 |

| 7 | Iowa | 66.6 |

| 8 | California | 66.5 |

| 8 | Georgia | 66.5 |

| 8 | Indiana | 66.5 |

| 8 | South Carolina | 66.5 |

| 12 | Pennsylvania | 66.2 |

| 12 | Washington | 66.2 |

| 14 | Illinois | 66.1 |

| 14 | Mississippi | 66.1 |

| 16 | Missouri | 66.0 |

| 16 | Ohio | 66.0 |

| 18 | New Jersey | 65.9 |

| 18 | Tennessee | 65.9 |

| 20 | Alabama | 65.8 |

| 20 | North Carolina | 65.8 |

| 20 | Texas | 65.8 |

| 23 | Michigan | 65.7 |

| 23 | West Virginia | 65.7 |

| 25 | Oregon | 65.6 |

| 25 | Virginia | 65.6 |

| 27 | Arkansas | 65.3 |

| 28 | Massachusetts | 65.1 |

| 28 | Nevada | 65.1 |

| 30 | Kentucky | 65.0 |

| 31 | Colorado | 64.8 |

| 31 | Wisconsin | 64.8 |

| 33 | Minnesota | 64.6 |

| 33 | Nebraska | 64.6 |

| 35 | Kansas | 64.5 |

| 36 | New York | 63.7 |

Florida, California metros take out the longest loans

We also looked at auto loan terms across metros. Among the 25 largest, Orlando (68.9 months) and Tampa (68.4) took out the longest auto loans, on average. They were followed by Riverside, Calif., at 67.6.

Given Florida finished at the top of our state rankings, it makes sense that two of its metros would lead this list. (Miami wasn’t far behind, at 66.8 months.) Median gross rent is higher in Orlando than in Tampa, plus Orlando’s residents earn slightly less, on average, than Tampa’s.

And while Californians have a higher per-capita income than the U.S. average, Riverside residents’ per-capita income is lower than the national average. That, plus a higher median gross rent total than the U.S. average, means Riverside residents are less likely to be able to afford shorter loan terms.

Metros where consumers take out the longest auto loans

| Rank | Metro | Avg. auto loan term (months) |

|---|---|---|

| 1 | Orlando, FL | 68.9 |

| 2 | Tampa, FL | 68.4 |

| 3 | Riverside, CA | 67.6 |

| 4 | Portland, OR | 67.4 |

| 5 | San Diego, CA | 67.0 |

| 6 | Miami, FL | 66.8 |

| 6 | St. Louis, MO | 66.8 |

| 8 | Phoenix, AZ | 66.6 |

| 8 | Charlotte, NC | 66.6 |

| 10 | Baltimore, MD | 66.4 |

| 11 | San Antonio, TX | 66.3 |

| 12 | Chicago, IL | 66.2 |

| 12 | Atlanta, GA | 66.2 |

| 14 | Houston, TX | 65.9 |

| 14 | Seattle, WA | 65.9 |

| 16 | Dallas, TX | 65.8 |

| 17 | Los Angeles, CA | 65.7 |

| 17 | Philadelphia, PA | 65.7 |

| 19 | Denver, CO | 65.5 |

| 20 | Washington, DC | 65.4 |

| 21 | San Francisco, CA | 65.1 |

| 21 | Detroit, MI | 65.1 |

| 23 | New York, NY | 64.5 |

| 23 | Minneapolis, MN | 64.5 |

| 25 | Boston, MA | 64.1 |

At the other end of this list were Boston (with an average term of 64.1 months) and Minneapolis and New York City (tied at 64.5).

The median gross rent in Minneapolis is comparable to the U.S. average, though Boston and New York have significantly higher median gross rent costs.

That said, the median annual household income for all three is at least as good as the U.S. average, and significantly higher for those in Boston. So that could help make those shorter loan terms possible for borrowers in those metros.

Portland, Ore., borrowers have the top share of long loans

Another way to consider this data is to look at the share of loans that exceeded six years (or 72 months) within a given metro.

Portland, Ore., emerged as the metro with the highest rate of borrowers taking on auto loans of more than six years, at 17.7%. This is a bit of an anomaly: Although residents tend to earn more than the national average, the median gross rent is also higher than the national average. This could suggest a wider split between those making those higher salaries compared to those earning below the median, leading to more people taking out longer loans.

After Portland, two Florida metros we’ve already mentioned — Tampa (16.7%) and Orlando (16.2%) — had the next highest proportions of these longer-term loans.

Metros with the highest share of auto loan terms longer than 6 years

| Rank | Metro | % of auto loan terms longer than 6 years |

|---|---|---|

| 1 | Portland, OR | 17.7% |

| 2 | Tampa, FL | 16.7% |

| 3 | Orlando, FL | 16.2% |

| 4 | Phoenix, AZ | 15.2% |

| 5 | Atlanta, GA | 14.9% |

| 6 | Baltimore, MD | 14.7% |

| 7 | Riverside, CA | 14.3% |

| 8 | Detroit, MI | 14.2% |

| 9 | Houston, TX | 13.8% |

| 9 | St. Louis, MO | 13.8% |

| 11 | Chicago, IL | 13.4% |

| 12 | Washington, DC | 13.2% |

| 13 | Charlotte, NC | 12.3% |

| 14 | Dallas, TX | 12.2% |

| 15 | Seattle, WA | 12.1% |

| 16 | New York, NY | 11.8% |

| 16 | Denver, CO | 11.8% |

| 18 | Miami, FL | 11.7% |

| 18 | San Diego, CA | 11.7% |

| 20 | Philadelphia, PA | 11.6% |

| 21 | San Francisco, CA | 11.2% |

| 21 | Minneapolis, MN | 11.2% |

| 23 | San Antonio, TX | 10.9% |

| 24 | Los Angeles, CA | 10.8% |

| 25 | Boston, MA | 8.2% |

At the other end of the spectrum, Boston (8.2%) was the only one of the 25 metros below 10.0%, which again makes sense given the metro’s place on our average term rankings. Above Boston, the next lowest percentages were Los Angeles (10.8%) and San Antonio (10.9%).

In some ways, Los Angeles is in a similar situation as Portland since the metro is also home to higher-than-average incomes paired with costlier rent prices. Again, the proportions of those earning those higher salaries may help explain why Los Angeles residents tend to get shorter auto loan terms. For example, the median value of owner-occupied housing units (including houses, condos and the like) is $822,600 in Los Angeles, compared to the $281,900 national average. So it’s possible that a larger segment of those taking out loans are in a solid financial position to afford shorter terms.

Interestingly, San Antonio is the opposite of Los Angeles in that residents earn less than the national average, but they also pay less in rent. Given that the average term in the metro is slightly higher than in Los Angeles, it makes sense that it would rank so closely here.

Tesla borrowers take out the longest auto loans

We also examined the 25 brands with the most auto loans closed on the LendingTree platform within the examined three years. Here, Tesla buyers took out the longest auto loans (70.0 months). That was followed by Kia (68.8) and Ram (67.9).

Given the high potential cost of new Teslas (which can run from about $40,000 to almost $110,000 based on the style) and the potential for significant tax credits when you buy qualifying electric vehicles, it makes sense that folks might look to finance their purchases — and take longer terms in exchange for those perks.

Despite Kia’s reputation as a value brand, its vehicles can go for above sticker price thanks to their popularity. That, along with increases in new car prices, means the cost has had room to rise. For example, the 2023 Kia Sorento Plug-In Hybrid starts at about $50,000.

Similarly, Rams also tend to run quite expensive, with the 2023 Ram 1500 having a sticker price ranging from about $42,000 to $86,000.

Average auto loan terms (by brand)

| Rank | Make | Avg. auto loan term (months) |

|---|---|---|

| 1 | Tesla | 70.0 |

| 2 | Kia | 68.8 |

| 3 | Ram | 67.9 |

| 4 | GMC | 67.3 |

| 5 | Hyundai | 67.2 |

| 6 | Nissan | 67.0 |

| 7 | Cadillac | 66.6 |

| 8 | Jeep | 66.5 |

| 9 | Chevrolet | 66.3 |

| 9 | Dodge | 66.3 |

| 11 | Ford | 66.0 |

| 12 | Infiniti | 65.9 |

| 13 | Volkswagen | 65.7 |

| 14 | BMW | 65.4 |

| 15 | Honda | 65.3 |

| 16 | Toyota | 65.2 |

| 16 | Audi | 65.2 |

| 16 | Mazda | 65.2 |

| 16 | Land Rover | 65.2 |

| 20 | Subaru | 65.0 |

| 20 | Acura | 65.0 |

| 22 | Porsche | 64.9 |

| 23 | Mercedes-Benz | 64.7 |

| 24 | Volvo | 64.6 |

| 25 | Lexus | 62.5 |

At the other end of the spectrum, Lexus (62.5 months), Volvo (64.6) and Mercedes-Benz (64.7) buyers had the shortest loan terms. Each has 2022 vehicles that start at or below $40,000 —though prices can vary greatly depending on the model and upgrades chosen, and older models will typically cost less.

Interestingly, Volvo and Mercedes-Benz have vehicles that could qualify for the electric vehicle tax credit. One explanation here could be that nonelectric models from those brands are more popular, and consumers may opt for shorter terms to control long-term costs.

4 tips to get out of auto debt

“With interest rates so high today, it’s likely not a great time to refinance your auto loan,” says Matt Schulz, LendingTree chief consumer finance analyst. “However, that doesn’t mean there’s nothing you can do.”

Here are four ways you can get a handle on car loan debt:

- Talk to your lender: If you’re having trouble making payments and don’t see those issues resolving in the near future, call your lender to discuss your options. As Schulz notes, it may be able to offer you a reprieve in the form of lower rates, deferred payments or other helpful changes.

- Consider renegotiating loan terms: If your credit has dramatically improved, your lender may be willing to look at your terms and adjust them. “Given how sharply auto loan rates have risen in such a short time, it may not help much,” Schulz says. “This move is far more likely to be impactful during a time of stable rates than during a period of rapid rate growth.” So you may want to wait for a better rate environment.

- Look into refinancing with a longer term: As seems to be the trend with new car loans, longer loan terms can help make monthly payments more affordable, meaning you’ll be more likely to stick to the projected payoff date. However, depending on when you refinance, that may mean you have to settle for higher rates (on top of the longer repayment timeline). So you’d pay more in the long term. Check that your current loan doesn’t have a prepayment penalty, which will make refinancing even more expensive.

- If all else fails, downgrade your vehicle: A car can be indispensable. But if you’re struggling to keep up with payments and have no other options, selling the car and getting an older (but still reliable) or smaller car can be the right financial move. Be sure to research the current estimated value of your car using a tool like Kelley Blue Book. That way, you can more accurately gauge your budget for the next one.

“Debt can be overwhelming, but it is important to understand that you have options,” he adds. “They may not be spectacular, but they are options nonetheless.”

Methodology

LendingTree analysts reviewed a sample of more than 20,000 auto loans closed on the LendingTree platform between Nov. 2, 2020, and Oct. 29, 2023.

Average loan lengths and the percentage of loans with terms of more than 72 months were aggregated across the 25 largest U.S. metros.

Auto loans were limited to car and light-truck purchases. Researchers excluded states or makes where samples were too low.

Get auto loan offers from up to 5 lenders in minutes